In this comprehensive Bilt 2.0 review, we analyze how the new cards finally invite homeowners to the party, ending the era where only renters had all the fun

On January 14, 2026, Bilt Rewards launched something that fundamentally changed the credit card landscape: three new cards that finally reward mortgage payments—an expense that has been a rewards dead zone since credit cards were invented.

Think about it: Your mortgage is likely your single largest monthly expense. For decades, major credit card issuers treated it like it didn’t exist. No points. No rewards. Just… payments into the void.

Until now.

Bilt 2.0 changes that. For the first time in credit card history, homeowners can earn unlimited points on mortgage payments with zero annual caps. Renters keep the perks they already have. And everyone gets access to a confusing-but-powerful new rewards currency called “Bilt Cash.”

This is a game-changer. But it comes with a catch that most people—and most blogs—don’t understand. That catch is a mechanism so confusing that some cardholders won’t use it, even though it’s genuinely valuable.

This guide decodes that mechanism. We’ll explain how “Bilt Cash” works, show you the exact math you need to know, and tell you which card is right for your situation. By the end, you’ll understand whether Bilt 2.0 is a no-brainer or a financial trap.

The 3 New Cards: Blue vs. Obsidian vs. Palladium

Bilt 2.0 gives you three distinct options. Choose based on your spending habits and priorities:

| Feature | Bilt Blue | Bilt Obsidian | Bilt Palladium |

| Annual Fee | $0 | $95 | $495 |

| Best For | No-fee simplicity / Students | The Sweet Spot for homeowners | Premium travelers / Heavy spenders |

| Welcome Bonus | $100 Bilt Cash | $200 Bilt Cash | 50,000 Bilt Points + $300 Bilt Cash + Gold Status |

| Base Earning | 1X points everywhere | 1X points + category bonuses | 2X points everywhere |

| Category Bonus | None | 3X dining OR grocery | None (flat 2X) |

| Grocery Earn | 1X | 3X (up to $25K/yr) | 2X |

| Dining Earn | 1X | 3X (unlimited) | 2X |

| Travel Earn | 1X | 2X | 2X |

| Rent/Mortgage Earn | 1X unlimited | 1X unlimited | 1X unlimited |

| Bilt Cash Back | 4% on non-housing | 4% on non-housing | 4% on non-housing |

| Annual Hotel Credit | None | $100 ($50 x2) | $400 ($200 x2) |

| Annual Bilt Cash | None | None | $200 |

| Airport Lounges | No | No | Yes (Priority Pass) |

| Great for Homeowners? | ✅ Yes (simplicity) | ✅✅ YES (value sweet spot) | ✅✅✅ Yes (premium experience) |

The “Bilt Cash” Mechanism Explained (The Key & Chest Analogy)

Here’s the part that confuses everyone. So we’re going to use a simple analogy.

The Old Bilt Card (Simplicity)

With Bilt 1.0, earning on rent was automatic. You charged rent, you got points. Like magic.

Think of it like paying with keys that automatically opened a treasure chest. No extra work required.

The New Bilt 2.0 System (Complexity + More Power)

With Bilt 2.0, the system is different. And it’s powerful, but it requires understanding the analogy:

Bilt Cash = The Key to the Treasure Chest Bilt Points = The Treasure Inside

Here’s how it works:

Step 1: You Earn Keys (Bilt Cash) on Everyday Spending

Every time you use your Bilt 2.0 card on groceries, dining, coffee, gas—basically anything that’s NOT rent or mortgage—you earn 4% back in Bilt Cash.

Example: Spend $100 on groceries → Earn $4 in Bilt Cash.

Those dollars are your “keys” to unlock something bigger.

Step 2: You Use Keys to Unlock the Treasure (Housing Points)

Here’s where the magic happens. When you pay rent or mortgage through Bilt, the system normally charges a 3% transaction fee (that’s standard for credit card mortgage/rent payments).

Bilt says: “Hey, we’ll let you use your Bilt Cash keys to pay that fee.”

So instead of paying $60 out of pocket for a $2,000 mortgage fee, you use $60 in Bilt Cash (the keys you earned), and you still get your 2,000 Bilt Points (the treasure).

Step 3: The Choice

If you don’t have enough Bilt Cash keys, you have three options:

- Pay the fee yourself ($60 on $2,000 mortgage) and still earn the points

- Skip the Bilt Cash entirely and earn zero points on that payment

- Spend more during the month to earn enough Bilt Cash to cover the fee next month

The Core Insight: Bilt Cash Unlocks Points Without Fees

This is the critical insight that separates “maximizers” from “average users”:

You can only earn fee-free housing points if you have Bilt Cash to cover the 3% transaction fee.

Without Bilt Cash, you either pay the fee or earn nothing.

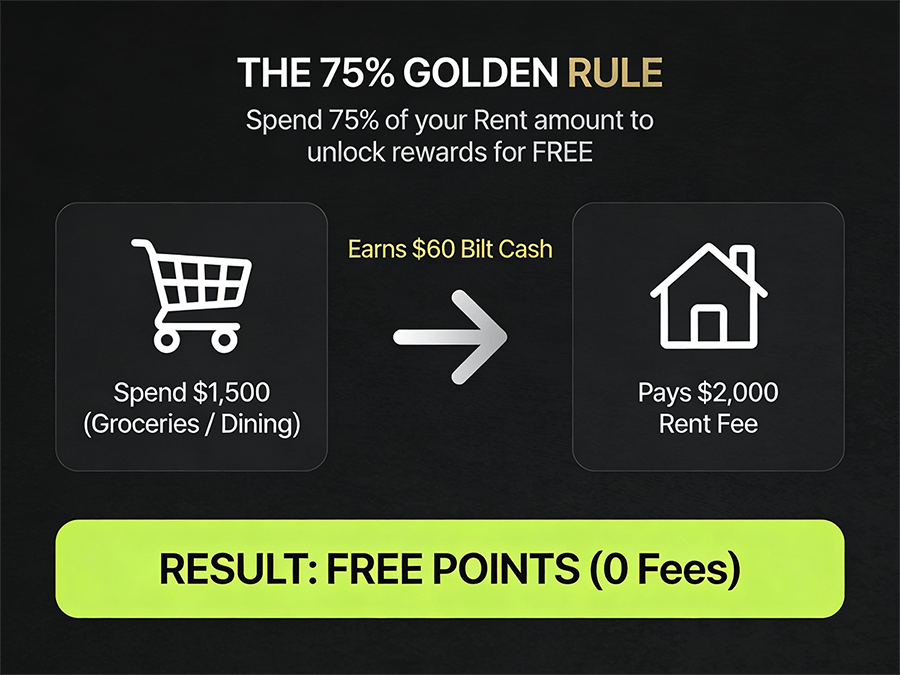

The “75% Rule”: Do You Spend Enough? (The Math Box)

This is the section that determines if Bilt 2.0 is actually worth your time. Let’s break down the exact math you need to know:

The Bilt Math: Why You Need to Spend 75% of Your Rent

Here’s the math that most people don’t understand:

You earn Bilt Cash at roughly 4% on everyday purchases (dining, groceries, gas, etc.). To unlock 1X points on your rent or mortgage without paying a 3% transaction fee, you need to spend approximately 75% of your housing payment amount on the card each month.

Why 75%? Because to unlock a $2,000 mortgage payment fee-free, you need $60 in Bilt Cash (3% of $2,000). To earn $60 at 4% back, you need to spend $1,500 ($60 ÷ 0.04 = $1,500). And $1,500 is 75% of your $2,000 mortgage.

Example: – Mortgage: $2,000 – Target everyday spend on card: ~$1,500 (75% of mortgage) – Bilt Cash earned: $60 (4% of $1,500) – Fee on mortgage: $60 (3% of $2,000) – Result: Fee is fully covered by Bilt Cash. You earn 2,000 points with ZERO out-of-pocket cost.

If you spend MORE than 75%: Let’s say you spend $3,000 on the card (not just $1,500). Now you earn $120 in Bilt Cash. You use $60 to cover the mortgage fee, and you still have $60 left over for other benefits (hotel credits, Lyft rides, etc.). Plus, you earn 3,000 bonus points from that $3,000 everyday spend.

If you spend LESS than 75%: Let’s say you only spend $500 on the card. You earn $20 in Bilt Cash. Your mortgage fee is $60. You’re $40 short. Now you either pay $40 out of pocket (reducing your “free” value), or you skip the housing payment through Bilt entirely (and earn zero points).

The Real-World Application

Let’s run the math for three scenarios:

Scenario A: Low Spender ($500 mortgage) – Monthly fee to cover: $15 (3% of $500) – Bilt Cash needed: $15 – Everyday spend required: $375 (to earn $15) – That’s 75% of your $500 mortgage ✓

Conclusion: Even renters with cheap housing can hit the 75% rule easily. This person just needs to spend $375/month on groceries/dining to earn fee-free housing points.

Scenario B: Mid-Range Homeowner ($2,000 mortgage) – Monthly fee to cover: $60 (3% of $2,000) – Bilt Cash needed: $60 – Everyday spend required: $1,500 (to earn $60) – That’s 75% of your $2,000 mortgage ✓

Conclusion: If you’re a normal homeowner, this math works perfectly if you spend $1,500/month on groceries, dining, and gas. Most people do.

Scenario C: High Spender ($4,000 mortgage) – Monthly fee to cover: $120 (3% of $4,000) – Bilt Cash needed: $120 – Everyday spend required: $3,000 (to earn $120) – That’s 75% of your $4,000 mortgage ✓

Conclusion: You need $3,000/month in everyday spend. That’s achievable for high earners, but it requires discipline.

Why 75% Matters

If you hit the 75% threshold, congratulations: You’ve cracked the code. You’re now earning unlimited points on your biggest monthly expense with zero fees. That’s genuine wealth creation.

If you fall short of 75%, you’re paying real money (3% fees) to earn points—which defeats the purpose.

The Three Cards: Which One Should You Choose?

Bilt Blue ($0 Annual Fee) — Best for Minimalists

Who: Renters, students, minimalists who want simplicity over optimization.

Why it works: 1X points everywhere + 4% Bilt Cash. If you hit the 75% rule (which is easy), you earn unlimited housing points with zero fees and no annual fee.

The math: A $2,000 renter who spends $1,500/month on food/gas earns: – 1,500 Bilt Points (everyday spend) – $60 Bilt Cash (to cover rent fee) – 2,000 Bilt Points (rent payment) – Total: 3,500 Bilt Points per month

That’s $52.50/month in travel value (at 1.5 cents per point) with zero annual fee. Solid.

The downside: No category bonuses. You’re leaving points on the table if you’re a heavy diner or grocery shopper.

Bilt Obsidian ($95 Annual Fee) — The Sweet Spot ⭐

Who: Homeowners and renters who spend $500+ monthly on dining OR groceries. Anyone who values earning potential over simplicity.

Why it works: This is where the real value lives.

The earning structure: – 3X points on your choice of dining OR groceries – 2X points on travel – 1X on everything else – 4% Bilt Cash – $100 annual hotel credit – $200 Bilt Cash welcome bonus

The math that makes it worthwhile:

A homeowner with a $2,000 mortgage who spends $2,000 on groceries and $1,000 on other categories earns: – 6,000 Bilt Points (3X on $2,000 groceries) – 1,000 Bilt Points (1X on $1,000 other) – $280 Bilt Cash (4% of $7,000 total non-housing) – 2,000 Bilt Points (mortgage payment via Bilt Cash) – Total: 9,000 Bilt Points per month, or $135/month in value

Subtract the $95 annual fee ($7.92/month), and you’re netting $127/month in pure value. That’s $1,524/year in travel value from just the card’s earning structure.

The math for renters:

A renter paying $2,000 rent who spends $3,000 on food/dining earns: – 9,000 Bilt Points (3X on $3,000 dining) – $200 Bilt Cash (4% on $5,000) – 2,000 Bilt Points (rent payment) – Total: 11,000 Bilt Points per month, or $165/month

After the $95 fee, you’re netting $157/month in value. That’s $1,884/year.

Should you get it? Yes, almost certainly. The $95 fee breaks even in your first two months of spending if you hit your category. For anyone who spends $500+/month on food, this card pays for itself many times over.

Bilt Palladium ($495 Annual Fee) — Premium Only

Who: Frequent travelers with high income, people who spend $10,000+/month on their card and want to maximize every dollar.

Why it works: 2X points everywhere means you’re earning 2,000 Bilt Points on a $2,000 mortgage without any effort. Plus: – $400 annual hotel credit – $200 annual Bilt Cash – Priority Pass airport lounge access – Double earning on a $4,000 mortgage gets you 8,000 points/month

The math:

A high-earning professional with a $4,000 mortgage who spends $6,000/month on the card earns: – 12,000 Bilt Points (2X on $6,000 everyday) – $240 Bilt Cash (4% on $6,000) – 4,000 Bilt Points (mortgage payment) – $400 hotel credit – $200 annual Bilt Cash – Total: 16,000 Bilt Points per month, or $240/month in value

After the $495 annual fee ($41.25/month), you’re netting $199/month in value. That’s $2,388/year.

Should you get it? Only if you’re spending $8,000+/month and traveling frequently. Otherwise, the Obsidian is better.

Pros & Cons of Bilt 2.0

Pros: Why Homeowners Should Be Excited

✅ Mortgage rewards (UNPRECEDENTED) — For the first time ever, homeowners can earn unlimited points on mortgage payments. No annual caps. No limits on number of homes. This is genuinely revolutionary. A $2,000/month mortgage that generates 2,000 Bilt Points = $30/month in value, or $360/year, just from an expense you’re already paying.

✅ Strong earning rates on food — The Obsidian’s 3X on dining or groceries is competitive with premium cards from Chase and Amex. If you spend $2,000/month on groceries, you’re earning 6,000 bonus points = $90/month in value. That alone makes the $95 fee trivial.

✅ Excellent transfer partners — You can transfer Bilt Points to 20+ airlines (United, Southwest, Alaska, Cathay Pacific) and 5 hotel chains (Marriott, Hyatt, Hilton) at 1:1 rates. This gives you real flexibility.

✅ No foreign transaction fees — Travel internationally without extra charges.

✅ Smooth transition with no hard credit pull — Current Bilt cardholders can switch to Bilt 2.0 with only a soft inquiry. Your card number stays the same. Autopay doesn’t break.

✅ Unlock high credit limits — Many Bilt cardholders report receiving $20,000-$30,000 credit limits, which helps lower your overall utilization ratio. Higher credit limits can significantly lower your utilization ratio, which is a key factor in boosting your score. Read our guide on How to Increase Credit Score Fast to learn more.

✅ Fee-free housing payments with Bilt Cash — You can always pay rent or mortgage with zero fees if you have Bilt Cash to unlock points. No forced fees ever.

Cons: Why Some People Will Hate It

❌ Confusing “unlock” system — The Bilt Cash mechanism is genuinely confusing. It’s not “swipe card, get points.” You have to actively manage Bilt Cash and understand fee structures. This will frustrate people who want simplicity.

❌ You MUST spend actively — You can’t just sock drawer this card. If you only use it once a month for rent and nothing else, you won’t generate enough Bilt Cash to cover fees. The old card was better for lazy spenders.

❌ Grocery category cap — The 3X grocery category maxes at $25,000/year. After that, you drop to 1X. (Dining is unlimited.) Big grocery families might hit this cap.

❌ Bilt Cash expires — Bilt Cash expires at year-end. You can roll over $100, but the rest disappears. This forces you to use it or lose it.

❌ New issuer is unproven — Bilt is moving from Wells Fargo (massive, stable) to Cardless (smaller, newer). While Cardless is legitimate, there’s a stability risk.

❌ Removed simplicity from old card — The original Bilt card’s “5-transaction minimum per month” guarantee is gone. Now you need to spend 75% of your housing to unlock fee-free points. That’s a downgrade for low spenders.

❌ Requires active management — You need to track Bilt Cash balance, plan spending, and optimize categories. If you want a “set it and forget it” card, this isn’t it.

Bilt 2.0 vs. Bilt 1.0: What Changed?

| Feature | Bilt 1.0 | Bilt 2.0 |

| Mortgage Rewards | ❌ Not available | ✅ YES—unlimited points |

| Rent Earning | ✅ 1X automatic, no fees | ✅ 1X (requires Bilt Cash unlock) |

| Annual Fee Options | $0 only | $0, $95, or $495 |

| Welcome Bonus | ❌ None | ✅ All three cards |

| 5 Transaction Minimum | ✅ Required each month | ❌ Removed |

| Rent Day 2X Bonus | ✅ Doubled points on “rent day” | ❌ Removed |

| Everyday Earning | 1X base (or 3X/2X if lucky with timing) | 1X-2X base + 4% Bilt Cash |

| Rewards Currency | Bilt Points only | Bilt Points + Bilt Cash |

| Card Issuer | Wells Fargo | Cardless |

| Complexity | Low | Medium-High |

Bottom line: Bilt 2.0 is more powerful but more complex. You can earn more, but you have to work for it.

The Verdict: Should You Apply?

YES, Apply If You:

✅ Are a homeowner with a $1,500+ mortgage — This is a no-brainer. Even the $0 Blue card lets you earn points on your biggest monthly expense. Pick the Obsidian for real optimization.

✅ Spend $500+ monthly on dining or groceries — The Obsidian’s 3X category bonus alone covers the $95 fee and generates serious value.

✅ Travel 2+ times per year — Bilt’s transfer partners (United, Hyatt, etc.) are excellent. You can convert housing points + everyday points into luxury travel.

✅ Want to maximize an “unavoidable expense” — Your rent or mortgage is money you’re spending anyway. Earning points on it is free money.

✅ Are a current Bilt cardholder — You MUST switch by January 30, 2026. After that, you become a Wells Fargo Autograph card (different rewards program). Switching is free and takes 10 minutes.

NO, Don’t Apply If You:

❌ Only use your card once a month for rent/mortgage — You’ll fall short of the 75% rule and either pay fees or earn nothing. The old card was better for you.

❌ Spend less than $500/month on the card — You won’t generate enough Bilt Cash to unlock fee-free housing points. Stick with a simpler card.

❌ Hate complex reward systems — The Bilt Cash “unlock” mechanism requires active thinking. If you want “swipe and forget,” this isn’t your card.

❌ Are uncomfortable with Cardless as your card issuer — If you have loyalty to Wells Fargo, you might prefer stability over rewards.

Frequently Asked Questions

Q: Can I Keep My Old Wells Fargo Bilt Card?

A: No, not forever. On February 7, 2026, Wells Fargo automatically converts all old Bilt cards to “Autograph Visa” cards (different program, different rewards, you lose Bilt Points forever).

To keep Bilt Points, you MUST switch to one of the three Bilt 2.0 cards by January 30, 2026. The switch is free, uses only a soft pull, and your card number stays the same.

Bottom line: Switching is mandatory if you want to keep your rewards program.

Q: Does Bilt 2.0 Really Work for Mortgages?

A: Yes. Unlimited points, no annual caps, multiple homes, any lender. It’s legitimate and unprecedented in the credit card industry.

Q: Is Bilt Cash Different from Bilt Points?

A: Yes, totally different currencies.

Bilt Points = Traditional rewards points. Transfer to airlines, hotels, or redeem for travel.

Bilt Cash = A dollar-equivalent currency. Earn 4% on everyday spend. Use to unlock housing points, pay for Lyft rides, book hotels, or get other credits.

Think: Bilt Cash is the “fuel” that makes the engine run. Bilt Points are where you travel.

Q: How Much Bilt Cash Do I Need?

A: Use this formula:

Bilt Cash needed = (Housing payment × 0.03)

Example: $2,000 mortgage × 0.03 = $60 Bilt Cash needed

To earn $60 at 4% back: $60 ÷ 0.04 = $1,500 in everyday spend

If you spend $1,500+/month on groceries, dining, gas, etc., you’ll have enough.

Q: Is the Obsidian Really Worth $95/Year?

A: For most people, yes.

If you spend $500/month on dining or groceries alone, the 3X bonus generates 1,000 extra points/month = 12,000 extra points/year = $180 value (at 1.5 cents per point). The $95 fee leaves you $85 ahead, and you haven’t even factored in your mortgage or other spending yet.

Q: Can I Change Dining vs. Grocery on the Obsidian?

Yes, once per year. Choose what works for your household. Summer might be dining, winter might be groceries.

Q: What About International Travel?

A: No foreign transaction fees on any Bilt 2.0 card. Plus, you earn 2X on travel (Obsidian/Palladium), so international flights and hotels generate bonus points.

The Bottom Line

Bilt 2.0 is a game-changer for homeowners and high-spending renters.

If you have a mortgage, you’ve literally never had this opportunity before. Earning points on your biggest monthly expense is financial optimization disguised as a credit card.

If you’re a heavy diner or grocery shopper, the Obsidian ($95 fee) is a no-brainer. The category bonus alone justifies the cost many times over.

If you’re lazy or low-spending, the old Bilt card (or a simpler card) was better for you. The new system rewards active, intentional users.

The deadline is January 30, 2026. If you’re a current Bilt cardholder and don’t switch, your card becomes a Wells Fargo Autograph and you lose all Bilt rewards forever. That’s not an option.

Final Word from Deep Charaniya, FinanceString Founder

When I first analyzed Bilt 2.0, I thought it was overcomplicated. Then I ran the numbers on my own mortgage and realized: This is one of the best opportunities credit cards have ever offered homeowners.

A $2,000 mortgage generating 2,000 points per month (with zero effort if you use Bilt Cash strategically) is worth $360/year in travel value. For free. Just from an expense you’re already paying.

The Bilt Cash mechanism isn’t complicated—it’s actually elegant once you understand the 75% rule. And the Obsidian card is genuinely the best travel card for everyday earners who don’t want to spend $450-550 on a premium card.

My recommendation: If you own a home, apply for the Bilt Obsidian right now. If you rent and spend heavily on food, apply for the Obsidian too. If you’re neither, the Blue card is still solid.

But do something by January 30. Your old Bilt card is about to become worthless.

Time to cash in on your biggest monthly expense.