I still remember the embarrassment I felt 5 years ago when my car loan application was rejected. The banker looked at my 580 score and simply shook his head. I felt trapped. If you are reading this, looking for answers on how to increase credit score fast, believe me, I understand your frustration.

But here is the truth: A bad score is not a life sentence. Once I cracked the code, I realized that learning how to increase credit score fast is actually about knowing specific loopholes in the banking system, not just paying bills.

The worst part? I thought I was doing okay. I paid my bills. Sure, I was always maxing out my credit cards, but I paid them off eventually. And there was that one time I missed a payment—but just one. I had no idea that one miss combined with 90% credit utilization was destroying my financial credibility.

That rejection was humbling. But here’s what it taught me: your credit score doesn’t have to define you, and you absolutely can learn how to increase credit score fast if you know what actually works.

I spent the next 30 days implementing specific tactics that my financial advisor recommended. I’m not going to lie—some worked better than others. But within 3 months, my score jumped to 680. By month 6, I hit 740. A year later, I qualified for that car loan at a rate I could actually live with.

Looking back, the biggest lessons weren’t complicated. They were just specific. That’s what I want to share with you today.

Check Your Credit Report for Errors (The Basics)

Here’s something that shocked me: roughly one in five people have at least one error on their credit report. One in five. And here’s the kicker—most of them don’t even know it.

These aren’t always small mistakes either. I’ve heard stories of people marked as 30 days late on a payment they made on time. Others had accounts in collections from creditors they’d already dealt with. Errors can knock off serious points.

What you need to do:

Go to AnnualCreditReport.com. This is the official government site. It’s free. No hidden charges, no upsells. You can pull your full credit report from Equifax, TransUnion, and Experian all in one place.

Better yet? You can check once a week for free now. That’s 52 free reports a year if you want to monitor your progress.

- Visit the site

- Enter your personal info

- Request reports from all three bureaus

- Download and review each one carefully

How to dispute an error you find:

Correcting these mistakes is the first step anyone should take when figuring out how to increase credit score fast.

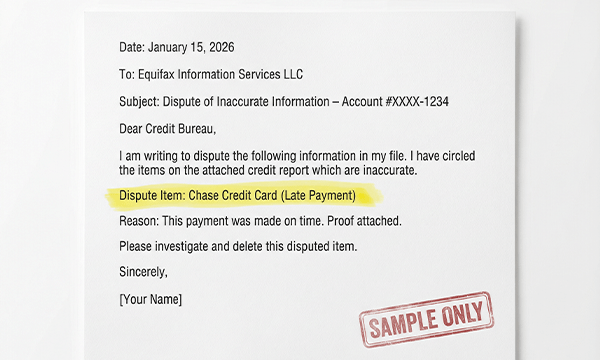

Let’s say you find a late payment that you know you made on time. Here’s exactly what to do:

- Get proof. Pull your bank records, canceled checks, or credit card statements showing the payment was made before the due date.

- Write to the bureau. You can do this online, via email, or certified mail. Be specific: “On [date], I paid $X for this account. Here is proof. This late payment is inaccurate.”

- Wait 30 days. The bureau legally has 30 days to investigate. They’ll either fix it or explain why it’s accurate.

- Check your report again. Make sure the correction shows up.

I know someone who found three errors this way. One was costing her about 15 points. Not huge, but when you’re trying to climb from 580 to 650, every point matters.

Pro Tip: Keep all your financial records organized. Bank statements, payment confirmations, receipts—store them. If you ever find an error, you’ll have proof ready to go.

Lower Your Credit Utilization Ratio (The 15/3 Hack)

Let me be straight with you: this is the single tactic that made the biggest difference for me.

Credit utilization is simple math. You have a credit limit. You use some of it. The percentage you use is your utilization ratio.

Example: $5,000 limit. $1,500 balance. That’s 30% utilization.

The problem? Most people think about this wrong. They think: “I’ll pay my bill on the due date, which is probably around the 25th of the month.”

Wrong timing. And here’s why it cost me.

Many experts agree that managing your utilization ratio is the mathematical secret to how to increase credit score fast without spending extra money

If your current credit card interest is too high, consider moving your debt to one of the Best Balance Transfer Credit Cards. This instantly lowers your utilization on the original card

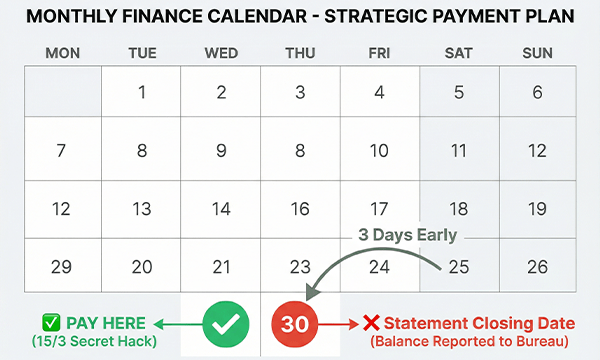

The Date Confusion That Kills Your Score

You have two dates:

- Statement closing date (when the credit bureau sees your balance)

- Due date (when you need to pay to avoid interest/late fees)

These are usually 20-30 days apart. Most people don’t realize this gap is their secret weapon.

The 15/3 Hack Explained

Here’s what changed everything for me: pay 15 days early, not on the due date.

Actually, let me be more specific. Pay 3 days before your statement closing date.

Let’s say your statement closes on the 15th of each month. Your due date is probably the 10th of next month. But the bureaus don’t care about that due date. They only see your balance on the 15th when your statement closes.

Real example from my life:

- Credit limit: $10,000

- Closing date: The 15th

- I had charged: $7,000 (that’s 70% utilization—ugly)

- Normally due date: Around the 9th of next month

Here’s what I did: On the 12th (3 days before closing), I paid $5,000. When the statement closed on the 15th, my balance showed as $2,000—just 20% utilization.

Could I pay the remaining $2,000 later? Absolutely. No interest. No late fees. But the bureaus already reported the 20% number.

Why this works:

Credit utilization is reported monthly. It updates to the bureaus within a week or so of your statement closing date. So you could see score improvement in 30 days—faster than almost any other single tactic.

For me, doing this on 3 different cards simultaneously brought my utilization down from 85% to 18%. My score jumped 40 points in 30 days.

Pro Tip: Set a calendar reminder for 3-4 days before your statement closing date. Many cards show this date on your statement or online. Set up automatic payments if you want to be hands-off about it. The key is making the payment before the statement closes, not before the due date.

Become an Authorized User (The “Piggybacking” Method)

This one feels almost like a cheat code. And honestly, it’s the fastest way to see real movement if you do it right.

Here’s how it works: You ask someone you trust—usually a parent, spouse, or close family member—to add you as an authorized user on their credit card account. You don’t need their signature. You don’t need to use the card. You just need to be added.

When that happens, their entire account history shows up on your credit report. Their payment history. Their account age. Their perfect 10% utilization. All of it.

I knew someone who did this with her mom’s American Express card. Her mom had a 750 credit score and 20 years of perfect payments. Within 45 days of being added, this person’s score jumped from 620 to 710. That’s a 90-point swing.

But here’s the critical part: This only works if the primary cardholder has solid credit.

If you don’t have time to wait for months, becoming an authorized user is often the most effective shortcut on how to increase credit score fast.

What You’re Actually Looking For

Before you ask someone, make sure they have:

- 7+ years of on-time payments. No missed payments. Not even one late.

- Low utilization. Below 10% if possible. Definitely below 30%.

- A credit score of 750+. You’re borrowing their good reputation. Make sure it’s actually good.

If the person you’re asking has a spotty payment history or high balances, being added to their account will hurt your score, not help it. I can’t stress this enough.

That’s why it has to be someone you trust completely. A parent, spouse, or very close friend who you know manages money responsibly.

What you need to do:

- Have the conversation. “Hey, I’m working on rebuilding my credit. Would you be willing to add me as an authorized user on one of your cards?”

- They call their credit card company and request you be added.

- Wait 30-45 days for the account to show up on your report.

- Your score starts benefiting immediately.

Pro Tip: Confirm with the cardholder before you do this that they understand: if they miss a payment or run up a balance after you’re added, it affects your score now too. You’re linked. Make sure they’re comfortable with that, and make sure you trust them.

Best Strategies on How to Increase Credit Score Fast (2026)

Now we’re getting into tactics that work alongside the main three.

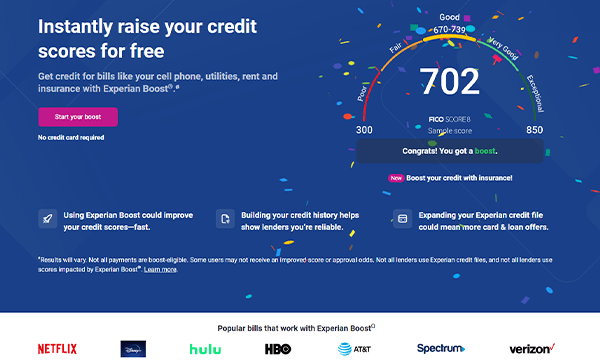

Experian Boost: The Free Tool Everyone Misses

Here’s something that blew my mind: your utility bills, Netflix subscription, and phone bill aren’t reported to credit bureaus by default. But they could be.

Experian Boost is a free tool that lets you add these payments to your credit file. Why does it matter? Because it shows you pay your obligations consistently.

What counts:

- Electric, gas, water bills

- Internet and cell phone bills

- Rent (if paid online)

- Insurance premiums

- Streaming services

How to use it:

- Go to Experian.com and find Boost

- Connect your bank account (it’s secure—bank-level encryption)

- Select which bills to add

- See your score update instantly

I added my utility and internet bills. My score went up about 8 points. Not massive, but combined with the other tactics, it added up. And it’s completely free and takes 5 minutes.

Lenders love to see a healthy mix of credit. Managing installment debts like Student Loans responsibly proves you can handle long-term financial commitments.

Don’t Close Old Credit Cards (Credit Age Is Real)

I know the temptation. Old card with an annual fee you don’t use? Close it, right?

Wrong. And I learned this the hard way.

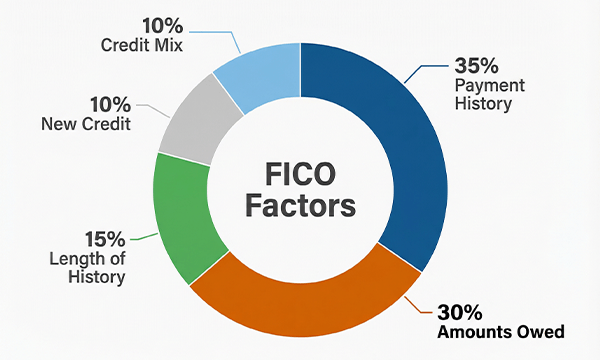

Your credit age—the average age of all your accounts—makes up 15% of your score. When you close your oldest card, that average age drops. Lenders see you as someone with a newer, riskier credit profile.

Plus, you lose available credit. If that old card has a $5,000 limit, closing it means your utilization ratio on your remaining cards jumps up.

What to do instead:

Keep the card open. If there’s an annual fee, call and ask for a waiver. I’m serious. Say: “I’ve had this card for 12 years and I want to keep it, but I don’t want to pay the annual fee. Can you waive it?”

Most of the time, they will. They’d rather waive $95 than lose a long-time customer.

If they won’t waive it, make one small purchase a year—buy a coffee with it. Keep it active. Pay the balance off. It costs you less than the annual fee is worth in credit score benefits.

Pro Tip: Never close an account in anger or frustration. That old card is working for you, even if you’re not using it. Think of it as paying a small price for credit score insurance.

The “Pay for Delete” Letter

This one is advanced because it doesn’t always work. But it’s worth trying, especially if you have collection accounts on your report.

Here’s the situation: You have a debt in collections. It’s hammering your score. You have the money to pay it, but paying it doesn’t remove it from your report—it just changes the status to “paid collection,” which still hurts.

Pay for delete is when you contact the collection agency and say: “I’ll pay you if you agree to delete this from my credit report completely.”

Why This Matters

Collections can knock 100+ points off your score. Even after paying, the account stays on your report for 7 years. That’s why deletion is worth negotiating for.

How to Actually Do It

Write a professional letter to the collection agency. Here’s what to include:

- Your name, address, phone number

- The account number

- The original creditor name

- Your settlement offer (usually 30-50% of what you owe)

- Your deadline (give them 15-30 days to respond)

Sample opening:

“I am writing to propose a settlement of this account. I am willing to pay $XXX in exchange for the complete deletion of this account from all three credit reporting agencies within 10 days of payment.”

Critical parts:

- Get it in writing. No verbal agreements.

- They must respond on company letterhead, signed by an authorized representative.

- You pay only after you have written confirmation.

- Use certified mail so you have proof they received it.

Be Real About the Odds

Here’s the honest part: many collection agencies won’t agree to this. Why? Credit bureaus are cracking down on it because it compromises the accuracy of reporting. Some agencies just don’t do it anymore.

But some will. Especially if you offer enough or if it’s older debt. And if they say no, you haven’t lost anything. You can always just pay and settle the account, which still shows responsibility to future lenders.Pro Tip: Never acknowledge the debt in your letter if you can avoid it. Say something like: “This letter is not an acknowledgment of debt, but rather a settlement proposal.” Your attorney can advise on this.

Frequently Asked Questions

Q: Is there really a way on how to increase credit score fast in 30 days?

A: Yes. By using the ‘Authorized User’ method or paying down your credit card balance 3 days before the statement date, you can see a significant jump in just one billing cycle.

Q: Can I Really Raise My Credit Score 100 Points in 30 Days?

A: Honestly? Sometimes. But not always. Here’s when it’s realistic:

When you CAN see 100 points in 30 days:

– You dispute and remove a major error (wrong late payment, identity theft)

You become an authorized user on an excellent account AND pay down high utilization

– You settle a serious collection account

– You had recent negative items removed

I know someone who had an account reported as 60 days late when they’d paid on time. Once that was corrected, their score jumped 85 points in 45 days.

When it takes longer:

If your low score is from recent late payments, expect 6-12 months of steady improvement

If you have limited credit history, building from zero takes time

If you have multiple collection accounts, removal takes negotiation

My honest answer? Multiple tactics working together create the fastest results. Just do one thing—pay down utilization—and you might see 20-30 points. But combine error disputes + utilization + authorized user + Boost, and you’re looking at 60-100 points in 30-45 days.

Q: Does Checking My Own Credit Score Hurt It?

A: No. Absolutely not. Stop worrying about this.

When you check your own score, it’s a soft inquiry. Soft inquiries have zero impact on your credit. You can check as often as you want—weekly, daily, whatever. No penalty.

The only inquiries that hurt are hard inquiries, and those only happen when you apply for a loan or credit card. Even then, it’s usually just a few points, and multiple inquiries for the same type of credit within 45 days count as one.

Check your score often. Track your progress. It helps you stay motivated. This is one place where you don’t need to second-guess yourself.

Pro Tip: Check once a month using free tools, or weekly if you want detailed tracking. Most credit card companies offer free score monitoring through their apps.

Final Thoughts

I’m not going to tell you this is easy. Rebuilding your credit takes work and discipline. But it doesn’t have to be complicated or mysterious.

Here are the three moves that mattered most for me:

1. Fix errors on your report (30-45 days). Go to AnnualCreditReport.com. Dispute any inaccuracies. This is the highest-impact, lowest-effort move.

2. Lower your utilization (30 days). Pay your bills 3 days before your statement closes instead of on the due date. This single tactic changed my trajectory.

3. Become an authorized user (30-45 days). Get added to someone’s excellent credit card account if you can. It’s like borrowing their credit history.

Add the free Experian Boost. Keep your old cards open. Maybe try a pay for delete letter if you have collections. And commit to paying on time going forward.

That’s it. Follow those steps, and you’ll have a completely different financial profile within 90 days.

Five years ago, I thought my credit score defined me. It felt permanent. But it wasn’t. When you know how to increase credit score fast, you realize your financial mistakes don’t have to be your future. You can change this. I did. And so can you.

Start today. Even if you just pull your free credit report and fix one error, you’re moving forward. That’s how this works—one step at a time.

Improving your score takes time. If you need cash urgently while you wait, check our curated list of Best Personal Loans for Bad Credit to get approved instantly.

Disclaimer: Credit improvement timelines vary based on individual circumstances. Results mentioned reflect real experiences but aren’t guaranteed for everyone. For personalized advice, consult a credit counselor or financial professional.