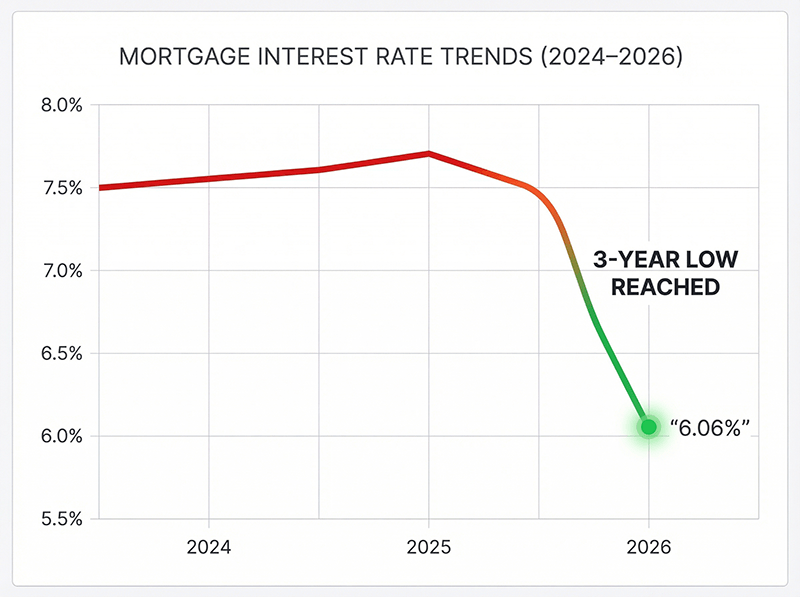

The massive mortgage rates drop 2026 has finally arrived, marking a turning point for millions of homeowners waiting on the sidelines. For the week ending January 15, the 30-year fixed-rate mortgage averaged 6.06%, according to Freddie Mac, marking its lowest level since early 2023. This represents a dramatic decline from the 7.04% rates homeowners faced just one year ago—a nearly one percentage point drop that translates to significant monthly savings for refinancers.

The question on every homeowner’s mind is simple: after years of frustratingly high rates, is now the time to refinance? The answer depends on several factors, but the data suggests conditions are more favorable than they’ve been since the pandemic era ended.

Analyzing the Mortgage Rates Drop 2026: How Low Are They?

To understand the significance of the current mortgage rates drop 2026, it’s essential to see how rates have evolved. The 30-year fixed-rate mortgage has fallen dramatically:

- Current (January 15, 2026): 6.06% (30-year), 5.38% (15-year)

- One year ago (January 2025): 7.04% (30-year), 6.27% (15-year)

- Peak in January 2025: 6.91–7.04%

- Lowest since 2023: Rates haven’t been this favorable in over three years

This mortgage rates drop 2026 wasn’t random. It followed the Federal Reserve’s three consecutive interest rate cuts in late 2025 (September, October, and December), combined with the Trump administration’s January 8 directive for Fannie Mae and Freddie Mac to acquire $200 billion in mortgage bonds to further reduce rates.

The 15-year fixed-rate option is equally attractive, standing at 5.38%—down nearly 89 basis points from the previous year. For borrowers prioritizing accelerated payoffs, this presents an exceptional opportunity.

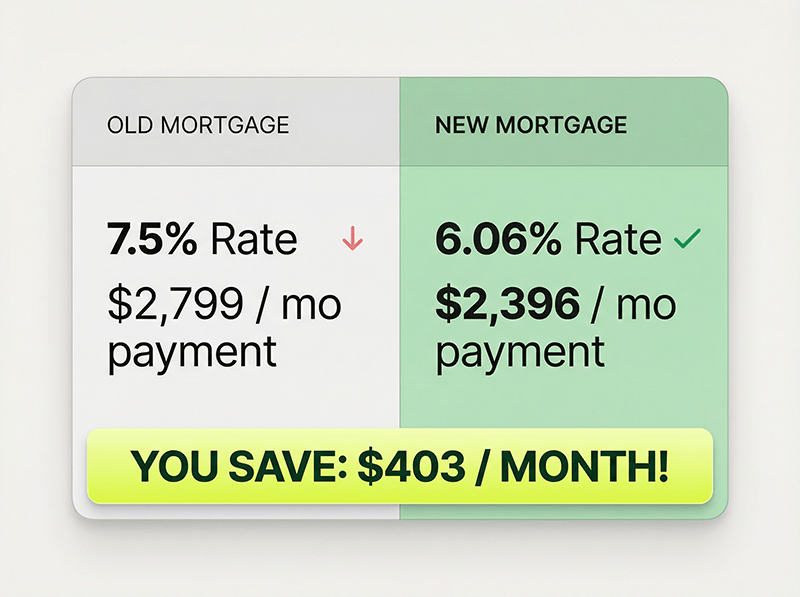

The Savings Calculation Table

Let’s put concrete numbers behind the mortgage rates drop 2026. For a homeowner with a $400,000 mortgage, here’s how refinancing from a typical 2025 rate to today’s rate changes the equation:

| Loan Amount | Old Rate (7.5%) | New Rate (6.06%) | Old Monthly Payment | New Monthly Payment | Monthly Savings | Annual Savings |

| $400,000 | 7.5% | 6.06% | $2,799 | $2,396 | ~$403 | ~$4,836 |

Over a 30-year loan, monthly savings of approximately $403 equates to cumulative interest savings of over $145,000.

This table illustrates why the mortgage rates drop 2026 has sparked a refinance rush. According to Freddie Mac, refinance applications have surged 133% year-over-year, and refinancing now represents 56.6% of all mortgage activity. The Mortgage Bankers Association projects refinance volume will exceed $670 billion in 2026—a 30% annual increase driven primarily by homeowners with rates locked in above 6%.

Who Should Refinance Now? (Checklist)

Not every homeowner should rush to refinance immediately. The mortgage rates drop 2026 creates opportunities, but timing requires strategic analysis. Use this checklist to assess whether refinancing makes sense for your situation:

Your refinance is likely worth pursuing if:

- Your current mortgage rate is 0.75% or higher above today’s rates (typically resulting in a break-even point under 24 months)

- You plan to stay in your home for at least 2–3 years beyond the break-even point

- Your credit score is 740 or above (optimal for conventional loans)

- You have at least 20% equity in your home

- Your debt-to-income ratio is 36% or lower

- Closing costs total less than 2.5% of your loan amount

Pause before refinancing if:

- Your current rate is only slightly higher (0.25–0.50%) than today’s rates

- You plan to sell or move within 2 years

- Your credit score has declined since your original mortgage

- You’re carrying significant consumer debt (refinancing may increase overall debt)

The “Break-Even” Point Explained

The break-even point determines when you’ll recoup refinancing costs. Here’s the formula:

Total Refinance Costs ÷ Monthly Savings = Months to Break-Even

For example, if refinancing costs $6,000 and you save $200 monthly, you’ll break even in 30 months (2.5 years). Typical refinance closing costs range from $4,000–$6,000, depending on your loan amount and lender.

Credit Score Requirements

Your credit score directly impacts the rates you qualify for. To maximize benefits from the mortgage rates drop 2026, aim for:

- Optimal range: 760–780 (best conventional rates)

- Good range: 740–759 (qualify for competitive rates)

- Acceptable range: 700–739 (rates still favorable)

- Minimum to qualify: 620 (rates significantly higher)

Even improving your credit score by 20–40 points can save thousands over the life of your loan. Need to boost your score? Start by reviewing how to increase your credit score fast, which covers debt reduction, payment history optimization, and error correction strategies.

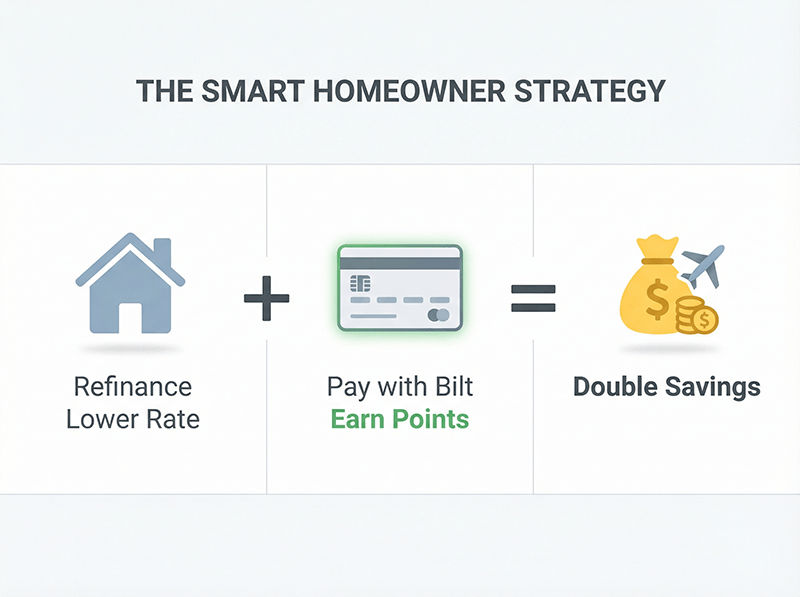

Double Your Profit: Refinance + Bilt Rewards

The mortgage rates drop 2026 combined with new rewards programs creates a unique opportunity to save money twice—once through lower rates and again through earning points on mortgage payments.

How It Works: The Bilt 2.0 Strategy

In January 2026, Bilt launched Bilt Card 2.0, a suite of credit cards that mark a game-changer for homeowners. For the first time, you can earn rewards on mortgage payments—specifically through the Bilt 2.0 credit card rewards program.

Here’s the dual-profit strategy:

Profit #1: Lower Your Monthly Payment

Refinance from a 7.5% rate to the current 6.06% rate on your $400,000 mortgage, saving approximately $403/month ($4,836/year) in principal and interest.

Profit #2: Earn Points on Mortgage Payments

With Bilt Card 2.0, you earn: – 4% Bilt Cash on everyday purchases (groceries, gas, utilities, etc.) – Up to 1 point per $1 on mortgage payments (converted from Bilt Cash with no transaction fee)

The mechanism works like this: For every $30 in Bilt Cash earned from everyday spending, you unlock 1,000 Bilt Points when making your mortgage payment. For a $2,000 monthly mortgage payment, you’d need $60 in Bilt Cash—achievable by spending approximately $1,500 on everyday purchases with your Bilt card.

The Rewards Cascade:

- Use Bilt Card for everyday expenses ($1,500/month) → Earn $60 Bilt Cash

- Apply $60 Bilt Cash to $2,000 mortgage payment → Unlock 2,000 Bilt Points (no fee)

- Redeem Bilt Points for travel, dining, fitness, or other benefits

According to Bilt’s data covering 5.5 million homes, this structure rewards 2 in 3 Bilt cardholders fully on housing payments. The Bilt Card also offers a 10% introductory APR on eligible purchases for 12 months, providing additional savings on everyday spending.

Expert Forecast: Will the Mortgage Rates Drop 2026 Continue?

As homeowners consider whether to lock in rates now, the critical question emerges: will the mortgage rates drop 2026 extend deeper into the year, or have rates bottomed out?

Professional Forecasts

Expert predictions suggest modest rate stability with slight downward movement:

- Freddie Mac / Federal Reserve: Rates expected to average around 6.0–6.3% through 2026

- Redfin: 6.3% average for entire year, with occasional dips below 6% but not sustained periods

- JP Morgan: ~6.3% average across 2026

- NAR (National Association of REALTORS): ~6.0% average for 2026, potentially unlocking 5.5 million additional qualified buyers

The Housing Market Forecast Supports Action Now

The broader housing market dynamics also support refinancing sooner rather than later:

1. Home Sales Rebound: NAR predicts a 14% increase in existing home sales for 2026, with purchase applications already up 31% year-over-year. This momentum suggests sustained housing activity through spring and summer.

2. Inventory Growth: Active listings are expected to increase 8.9% in 2026, with the months of supply averaging 4.6 (indicating a balanced market). More inventory means buyers have options, which could gradually improve borrower negotiating power.

3. Rate Stability Risk: While rates could dip slightly further, the consensus suggests they’ll hover near 6.0%–6.3% rather than plummet. Any further Fed rate cuts are unlikely—the Fed has signaled only one potential cut in 2026.

Should You Wait or Lock In Now?

The data suggests locking in now is prudent for most homeowners. Here’s why:

- Diminishing returns: The gap between 6.06% and potential future lows (5.8%–5.9%) is modest. Even a 0.2% rate drop on a $400,000 loan saves only $50–$60/month

- Closing costs: These fixed costs ($4,000–$6,000) mean you need significant rate improvement to break even. Waiting 6 months for 0.2% savings doesn’t justify another refinance cycle

- Lock-in certainty: Today’s rates guarantee savings vs. current payments. Future rates introduce risk and uncertainty

For homeowners with rates above 6.5%, the math strongly favors refinancing now to capture the mortgage rates drop 2026 before potential upward pressure returns.

Conclusion

The mortgage rates drop 2026 represents a watershed moment in the housing market, delivering relief after years of elevated borrowing costs. With 30-year fixed rates at 6.06%—the lowest since early 2023—homeowners can refinance into meaningful monthly savings while simultaneously earning rewards through innovative programs like Bilt Card 2.0.

The opportunity won’t last forever. As housing demand accelerates through spring and summer 2026, rate pressure may re-emerge. Refinance applications have already surged 133% year-over-year, signaling that savvy homeowners recognize the window. The combination of the mortgage rates drop 2026 with a robust housing market recovery and rewards-on-mortgage credit cards creates a rare alignment of advantages.

If your credit score exceeds 740 and your current rate exceeds 6.5%, the decision is clear: lock in today’s rates and capture the dual benefits of lower monthly payments and mortgage rewards.