Key Takeaways

- Lower interest rates available: Current fixed rates start as low as 3.01% APR (through marketplace lenders) to 3.99% APR (from major lenders), depending on your credit profile, loan amount, and repayment term. Qualifying borrowers could save thousands in interest.

- Eligibility requirements: Most lenders require a credit score of 670+, stable income of at least $35,000, and a minimum loan balance of $5,000-$10,000

- Processing timeline: The entire refinancing process typically takes 2-4 weeks, though it can extend to 2-3 months with additional document verification

- Critical trade-off: Refinancing federal student loans means permanently losing access to income-driven repayment plans, Public Service Loan Forgiveness, and other federal protections

- Top lenders in 2026: Earnest, ELFI, SoFi, Laurel Road, and LendKey all offer competitive rates with refinancing bonuses up to $1,250

- Refinancing works best for: Those with private student loans, good credit, stable employment, and no plans to use federal loan forgiveness programs

- Best rate type: Most borrowers benefit from fixed-rate refinancing for predictability, though variable rates may suit those planning quick repayment

Are you drowning in student loan debt with monthly payments that seem impossible to manage? You’re not alone. Millions of Americans carry an average of $37,574 in student loan debt, and many are paying interest rates that are significantly higher than what’s available today.

Student loan refinancing offers a powerful solution. By refinancing your student loans in 2026, you could potentially lower your interest rate by 2-3 percentage points, reduce your monthly payment, and save tens of thousands of dollars over the life of your loan. A borrower with $100,000 in student loans at 7% interest could save over $50,000 by refinancing to a 4% rate on a standard 10-year term.

But refinancing isn’t right for everyone. The decision to refinance student loans requires careful consideration of your financial situation, loan type, and long-term goals. This comprehensive guide will walk you through everything you need to know about how to refinance student loans in 2026, including the step-by-step process, eligibility requirements, top lenders, and critical factors to consider before making your decision.

What Does It Mean to Refinance Student Loans?

Student loan refinancing is the process of taking out a new loan from a private lender to pay off one or more existing student loans. When you refinance, your new private lender pays off your current loan balance, and you then make payments on the new loan instead.

The primary goal of refinancing is to secure better loan terms than your current loans offer. This typically means:

- Lower interest rates for reduced monthly payments and total interest paid

- Shorter repayment terms to become debt-free faster

- Simplified repayment by consolidating multiple loans into a single payment

- Changed loan terms to better fit your current financial situation

Important distinction: Refinancing is different from consolidation. When you consolidate federal student loans, you combine them into a single Direct Loan through the federal government at the weighted average of your existing rates. Refinancing, on the other hand, involves taking out a private loan, which may offer a lower rate but causes you to lose federal protections.

Should You Refinance Your Student Loans? Key Considerations

Before you start the refinancing process, ask yourself these critical questions:

Do You Have Private Student Loans?

The safest candidates for refinancing are those with private student loans. Private loans don’t offer the federal protections that make refinancing risky. If you’re paying 8-10% on private loans, refinancing to a lower rate is almost always beneficial.

Are Your Federal Loans Worth Keeping?

If you have federal student loans, the decision becomes more complex. Federal loans come with significant protections that you’ll permanently lose by refinancing:

- Income-driven repayment (IDR) plans that cap your monthly payment at 10-20% of discretionary income

- Public Service Loan Forgiveness (PSLF) that forgives remaining balance after 10 years of qualifying payments in government or nonprofit work

- Teacher Loan Forgiveness programs

- Deferment and forbearance options during financial hardship

- Death and disability discharge protection

- Future forgiveness programs that the government may offer

If you work in public service, plan to pursue loan forgiveness, or expect income fluctuations, keeping your federal loans is likely the better choice—even if it means paying a slightly higher interest rate.

How Strong Is Your Credit?

Refinancing is a credit-based process. Most lenders require a credit score of 670 or higher to qualify for the best rates. If your credit score is below 650, you may still qualify but at higher interest rates, potentially negating any refinancing benefit. If you’re in this situation, consider taking 6-12 months to improve your credit before refinancing.

Do You Have Stable Income and Employment?

Lenders want assurance that you can make your payments. They’ll review your income history and current employment stability. If you’re self-employed, recently changed jobs, or have irregular income, you may need a cosigner or may not qualify for the lowest rates.

Eligibility Requirements: Do You Qualify?

Most student loan refinance lenders have similar eligibility criteria. While requirements vary slightly by lender, here’s what you’ll typically need:

| Requirement | Details |

| Credit Score | 670-680 minimum; 700+ unlocks best rates (some lenders accept 580+) |

| Credit History | Minimum 36 months of credit history required |

| Minimum Income | Typically $35,000-$50,000 annually |

| Minimum Loan Amount | $5,000-$10,000 (lenders set different minimums) |

| Education | Bachelor’s degree or higher from eligible Title IV school |

| Citizenship | U.S. citizen or permanent resident alien |

| Employment | Steady employment history preferred |

| Debt-to-Income Ratio | Generally 40% or lower is preferred |

What If You Don’t Meet All Requirements?

Add a cosigner. If you’re just short of meeting eligibility requirements, bringing on a qualified cosigner (typically a spouse, parent, or family member with strong credit) can help you qualify. More importantly, a cosigner with excellent credit can help you secure a significantly lower interest rate—potentially 0.5-1% lower.

Current Student Loan Refinance Rates in 2026

Interest rates for student loan refinancing fluctuate based on market conditions, your credit profile, and the lender. Here’s what’s currently available:

Fixed-Rate Loans

Fixed-rate loans offer interest rate stability and predictable monthly payments. Current fixed-rate refinance APRs range from 3.01% to 9.99%, depending on creditworthiness and loan terms.

For a $100,000 loan over 10 years: – At 3.01%: Monthly payment of $960; Total interest of $15,000 – At 5.50%: Monthly payment of $1,056; Total interest of $26,700 – At 9.99%: Monthly payment of $1,387; Total interest of $66,400

Variable-Rate Loans

Variable-rate loans typically start lower than fixed rates but can increase over time. Current variable-rate refinance APRs range from 3.03% to 11.41% (with rate caps). These loans are best for borrowers planning to pay off their loans quickly or those comfortable with interest rate risk.

Comparison of Fixed vs. Variable: – Fixed rates provide budget predictability – Variable rates offer initial savings if rates stay low – Variable rates carry interest rate risk if the market rises

Step-by-Step Guide: How to Refinance Student Loans

Step 1: Assess Your Current Loan Situation

Before you apply, gather complete information about your existing loans:

- Total loan balance(s)

- Current interest rates

- Current monthly payment

- Remaining repayment term

- Loan servicer information

- Current lender contact details

Pro Tip: Calculate your break-even point. The refinancing process has transaction costs (though most lenders don’t charge upfront fees). Will your interest savings justify these costs? As a general rule, refinancing makes sense if you’ll keep the new loan for at least 2-3 years.

Step 2: Research and Compare Lenders

This is critical. Don’t apply with just one lender. Each lender uses slightly different credit assessment methods, and your rate quote can vary by 1-2% between lenders.

Top refinancing lenders to research:

- Earnest: Best for Precision Pricing (custom terms)

- SoFi: Competitive rates and no origination fees

- ELFI: Strong for parent PLUS refinancing and customer service

- College Ave: 11+ repayment term options (5-15 years)

- Laurel Road: Specializes in healthcare professionals

- LendKey: Marketplace connecting to community banks and credit unions

- Credible: Shopping platform comparing multiple lenders

Use rate comparison tools (without hard credit pulls) to understand your likely rate range before applying.

Step 3: Pre-Qualify to Estimate Your Rate

Pre-qualification takes just 2-5 minutes and doesn’t impact your credit score. Enter basic information (income, loan balance, credit score range) to see estimated rates and terms you might qualify for.

During pre-qualification, most lenders will offer multiple repayment term options (5, 7, 10, 15, or 20 years) with corresponding rate estimates. Choose a few scenarios to evaluate:

- Shorter term (5-7 years): Higher monthly payment, lower total interest

- Standard term (10 years): Balanced payment and interest savings

- Longer term (15-20 years): Lower monthly payment, higher total interest

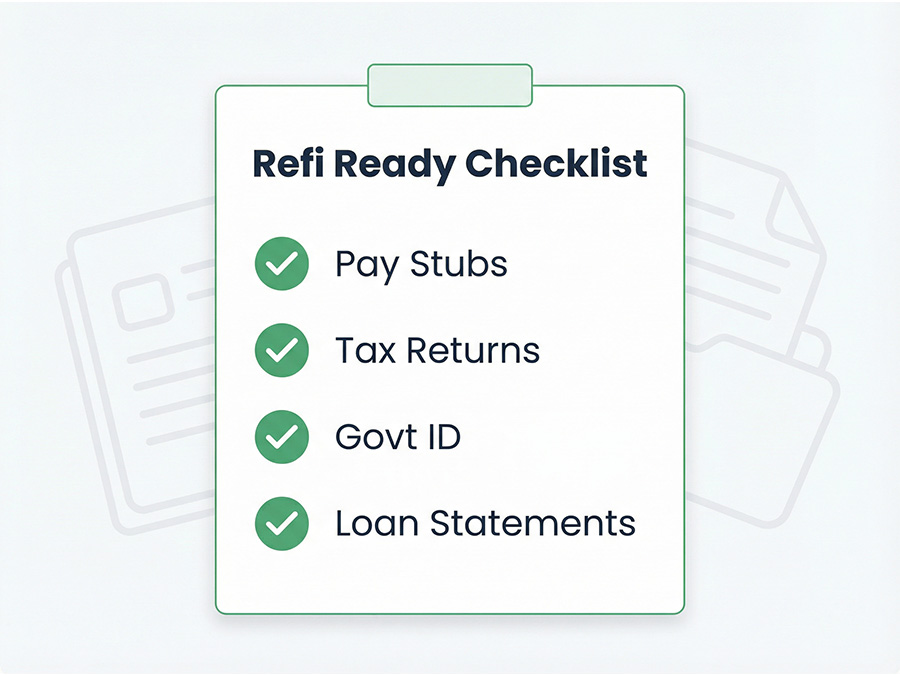

Step 4: Gather Required Documentation

Before submitting a full application, prepare these documents. Having them ready speeds up the process:

Financial Documents: – Pay stubs (last 2 months) – Tax returns (last 2 years) – W-2 forms or 1099s (proof of income) – Bank statements (proof of assets)

Identification: – Government-issued ID – Social Security number – Date of birth

Loan Information: – Current loan statements or payoff quotes – Proof of graduation/degree – Proof of employment

If Applying with a Cosigner: – All of the above for the cosigner as well – Authorization for cosigner’s credit pull

Step 5: Submit Your Full Application

Once pre-qualified and documents are ready, submit your complete refinancing application. This typically involves:

- Fill out the online application: Personal information, employment history, income, loan details (15-20 minutes)

- Authorize a hard credit pull: This will temporarily lower your credit score by 5-10 points but will recover within 30 days

- Upload documents: Use your lender’s portal to upload required documentation (photos or PDFs)

- Select your loan terms: Choose your preferred interest rate type (fixed or variable) and repayment term

Step 6: Underwriting and Verification (1-10 Business Days)

After you submit, the lender’s underwriting team reviews your application:

- Verify income from your tax returns and recent pay stubs

- Confirm employment history

- Review debt-to-income ratio

- Contact previous lenders to verify loan balances

- Complete a full credit evaluation

If everything checks out, you’ll receive conditional approval or a formal loan offer within 1-10 business days.

If they need clarification, the lender will contact you (usually within 2-4 business days) to request additional documents or information.

Step 7: Review and Sign Your Loan Agreement

Once approved, you’ll receive:

- Loan estimate/offer: Shows interest rate, monthly payment, total interest over loan life, fees, and terms

- Loan disclosure: Federal disclosures about your loan terms and rights

- Note and promissory agreement: The legal contract

Important: You have a 3-day rescission period (after signing the disclosure) to cancel without penalty. Use this time to:

- Verify all loan terms match your offer

- Confirm the interest rate and monthly payment

- Review any fees

- Ask final questions

Step 8: Loan Funding and Payoff (2-6 Weeks After Signing)

Once you’ve signed final documents and the rescission period passes:

- The new lender obtains final payoff quotes from your current lender(s)

- Funds are sent to pay off your existing loan(s)

- You receive confirmation that your old loans are paid in full

- You begin making payments to your new lender

Critical reminder: Continue making payments to your current lender until you receive confirmation that the refinancing is complete. Any overpayments will be refunded or applied to your new loan.

Comparison Table: Top Student Loan Refinance Lenders (2026)

| Lender | Best For | Fixed APR | Variable APR | Min. Loan | Bonus | Terms |

| Earnest | Custom terms & low income | 3.72–9.99% | 5.88–9.99% | $5,000 | $0-$500 | 5-20 years |

| SoFi | Competitive rates & perks | 4.24–9.99% | 5.99–9.99% | $5,000 | $500 ($100k+) | 5-20 years |

| ELFI | Parent PLUS & service | 4.88–8.44% | 4.74–8.24% | $10,000 | $300-$1,099 | 5-15 years |

| College Ave | Flexible terms | 4.74–8.75% | 5.04–9.05% | $5,000 | $0-$300 | 5-15 years |

| Laurel Road | Healthcare professionals | 4.25–10.24% | 4.86–10.24% | $5,000 | $300-$500 | 5-15 years |

| LendKey | Credit unions & banks | 4.54–9.04% | 4.50–9.27% | $5,000 | $100-$1,250 | 5-20 years |

| Credible | Rate shopping | 3.01–10.15% | 3.03–11.41% | $5,000 | Up to $1,250 | 5-20 years |

Note: Rates are estimates as of January 2026 and vary based on credit profile, income, and loan term. Actual rates offered depend on individual qualification.

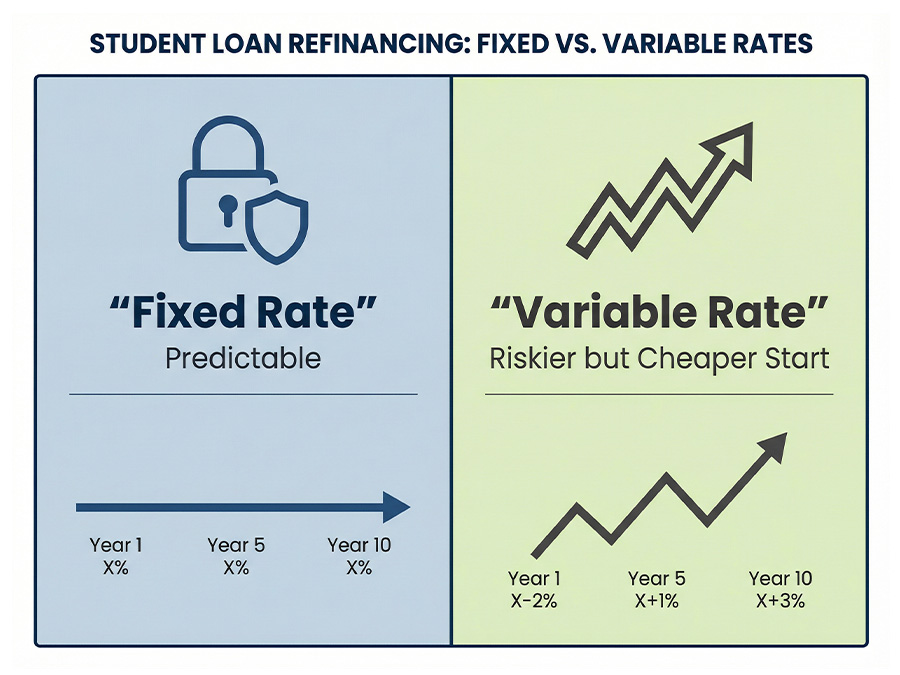

Critical Decision: Fixed vs. Variable Interest Rates

This choice dramatically affects your long-term cost:

Fixed-Rate Loans

Best for: Most borrowers, especially those staying in a loan 5+ years

Advantages: – Interest rate locked for entire loan term – Monthly payment never changes – Perfect for budgeting and financial planning – Protection against future rate increases

Disadvantages: – Usually starts 0.5-1% higher than variable rates – Higher total interest if rates decline significantly

Variable-Rate Loans

Best for: Borrowers planning to pay off loans quickly (2-3 years) or those comfortable with interest rate risk

Advantages: – Starts 0.5-1% lower than fixed rates – Significant interest savings if rates stay flat or decline – Potential to pay off loan faster

Disadvantages: – Rates can increase monthly or annually (depending on adjustment schedule) – Monthly payment can become unpredictable and increase substantially – Higher risk of paying more total interest if rates rise sharply – Difficult to budget with payment uncertainty

Rate Caps Matter: If choosing variable, check the rate cap (maximum rate the loan can reach). A variable loan capped at 9.99% is safer than one capped at 13.95%.

FinanceString Expert Tip: The Pre-Qualification Power Play

Here’s a refinancing strategy that most borrowers miss: Pre-qualify with 3-5 lenders simultaneously during the pre-qualification phase (which doesn’t damage your credit).

During the week you plan to refinance, submit full applications with 2-3 top-rated lenders. Multiple credit inquiries within 14 days typically count as ONE inquiry for credit scoring purposes. This gives you the power to:

- Compare actual (not estimated) rate offers side-by-side

- Negotiate with lenders (“Lender A offered 4.2%, can you match that?”)

- Collect multiple refinancing bonuses (often $100-$500 each)

- Choose the absolute best deal based on real numbers

Many borrowers stop after one application and miss savings of $1,000+ by not seeing what other lenders offer.

Important Federal Loan Changes in 2026: How They Affect Your Decision

Starting July 1, 2026, major changes take effect for new federal student loan borrowers under the One Big Beautiful Bill Act:

| Change | Impact |

| Two repayment options only | New borrowers get Standard Plan (10 years) or Repayment Assistance Plan (RAP—30 years with income adjustment) |

| Grad PLUS loans eliminated | Graduate students lose access to these higher-amount loans |

| New borrowing caps | Strict limits on how much graduate/professional students can borrow |

| Reduced hardship protections | Fewer deferment and forbearance options after July 2027 |

What this means for refinancing decisions: With federal loans becoming less flexible and offering fewer protections, some borrowers may find private refinancing more appealing. However, those pursuing Public Service Loan Forgiveness or expecting income fluctuations should still maintain federal loans despite these changes.

Major Pros and Cons of Student Loan Refinancing

Advantages of Refinancing

Lower Interest Rates

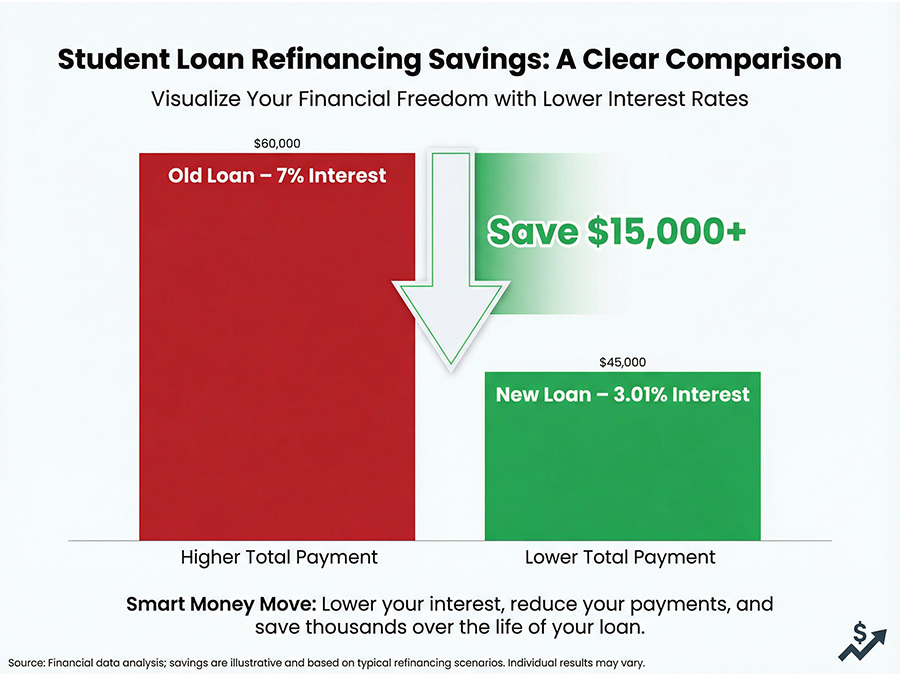

The primary benefit: If you have federal loans at 6.39-8.94% or private loans at 7-10%, refinancing to 4-5% saves significant money. On a $50,000 loan, dropping from 7% to 4.5% saves over $15,000 in interest.

Reduced Monthly Payments

Lower rates mean lower monthly payments. Depending on your situation, this could free up $200-$500+ monthly for other financial goals.

Faster Debt Payoff

Choose a shorter repayment term (7 instead of 10 years) to become debt-free faster while saving interest.

Simplified Payments

Consolidate multiple loans into one payment with one due date, simplifying your financial life.

Cosigner Release Option

Some lenders offer cosigner release after several on-time payments, allowing you to remove a family member from the loan.

No Origination Fees

Most reputable lenders charge no upfront origination or application fees (unlike some other loans).

Disadvantages of Refinancing

Loss of Federal Protections (If Refinancing Federal Loans)

This is the critical drawback. You permanently lose: – Income-driven repayment options – Public Service Loan Forgiveness eligibility – Teacher Loan Forgiveness – Deferment and forbearance flexibility – Future government forgiveness programs

Once refinanced, you cannot convert back to federal loans.

Interest Rate Risk (With Variable Rates)

Variable-rate loans can increase if market rates rise. Your monthly payment could jump $200-$300+ if rates hit their caps.

Eligibility Requirements

You need good credit (670+), stable income, and sufficient loan balance. Not everyone qualifies for the lowest rates.

No Loan Forgiveness

Private lenders don’t offer loan forgiveness programs. Your loan must be repaid in full—there’s no 20-25 year forgiveness option like federal IDR plans.

When NOT to Refinance Student Loans

Refinancing isn’t the right choice if:

You work in public service or non-profit sector

Public Service Loan Forgiveness (PSLF) is worth potentially $100,000+ in forgiveness. Don’t give it up for a slightly lower rate.

You plan to pursue loan forgiveness

If forgiveness is in your 5-10 year plan, refinancing terminates that path permanently.

You expect income changes or job instability

Federal hardship protections, income-driven repayment, and forbearance are invaluable safety nets that private loans don’t offer.

You have significant federal loan benefits

If your federal loans have aggressive autopay discounts, principal rebates, or other special benefits, refinancing may not be worth it.

You can’t qualify for a lower rate

If you’d only qualify for rates similar to or higher than your current loans, refinancing is pointless.

You’ve already experienced federal loan forgiveness or discharge

Refinancing terminates your eligibility for future federal relief if circumstances change.

Common Refinancing Mistakes to Avoid

Mistake #1: Not Comparing Multiple Lenders

Rates vary by 1-2% between lenders. Applying with only one lender could cost you thousands. Solution: Get quotes from 3-5 lenders before deciding.

Mistake #2: Extending Your Loan Term Without Considering Total Interest

A longer term means lower monthly payments but significantly higher total interest. For example, extending a 10-year loan to 20 years can more than double total interest paid. Calculate the true cost before extending your term.

Mistake #3: Forgetting to Check for Fees

While most lenders don’t charge origination or application fees, some do. Ask explicitly about: – Origination fees – Application fees – Prepayment penalties – Administrative fees – Document preparation fees

Reputable lenders have ZERO fees. Move on if a lender charges upfront fees.

Mistake #4: Not Calculating Your Break-Even Point

Refinancing costs time and money to process. If you only keep the new loan for 1-2 years, you may not break even on the savings. Calculate: Will your interest savings within your expected timeframe exceed the transaction costs?

Mistake #5: Not Asking About Autopay Discounts

Many lenders offer 0.25% interest rate reductions for automatic payments. This 0.25% might not sound like much, but on a $100,000 loan, it saves $2,500 over 10 years.

Mistake #6: Ignoring Your Credit Score Before Applying

Your credit score determines your rate. If your score is below 650, you won’t qualify for the best rates. Improve your credit first by paying bills on time and reducing debt.

Mistake #7: Refinancing Federal Loans Without Fully Understanding the Consequences

This is the biggest mistake. Many borrowers refinance federal loans and later regret losing PSLF eligibility. Before refinancing any federal loans, research whether forgiveness programs might apply to you.

Mistake #8: Not Asking About Hardship Options

Even reputable private lenders have limited hardship, deferment, and forbearance options compared to federal loans. Ask specifically what happens if you lose your job or face financial hardship. Know your options before signing.

Frequently Asked Questions About Student Loan Refinancing

Q1: How long does the refinancing process take?

The process typically takes 2-4 weeks from application to loan funding, though it can extend to 2-3 months if additional document verification is needed.

Timeline breakdown: – Pre-qualification: 5 minutes – Full application: 15-20 minutes – Underwriting review: 1-10 business days – Document verification: 1-2 weeks – Final approval and signing: 2-3 days – Loan disbursement: 2-6 weeks after signing – Total: 2-4 weeks on average

Continue making payments to your current lender until you receive confirmation that the refinancing is complete.

Q2: Does refinancing hurt my credit score?

Yes, initially—but only temporarily. When lenders perform a hard credit pull (required for refinancing), your credit score typically drops 5-10 points. However, your score rebounds within 30 days as you demonstrate responsible management of the new loan.

Tip: Avoid applying for other credit (credit cards, car loans, mortgages) within 30 days of refinancing to minimize credit damage.

Q3: Can I refinance if I have bad credit?

Most lenders require a credit score of 670+. However, you have options:

Add a cosigner with good credit to qualify

Wait 6-12 months while improving your credit score (pay all bills on time, reduce credit card balances)

Look for lenders with lower minimums (some accept 620-630)

Refinance later when your credit improves

If you’re forced to refinance with bad credit, the rates will be higher, potentially eliminating refinancing benefits.

Q4: Can I refinance only some of my loans?

Yes. You can refinance individual loans or groups of loans while leaving others alone. For example, you might refinance only your private loans while keeping federal loans with forgiveness potential.

However, refinancing one loan at a time may be inefficient if you’re dealing with consolidation fees or application processes. Most borrowers refinance all private loans together.

Q5: How many times can I refinance my student loans?

Unlimited. Some borrowers refinance multiple times as rates drop or their financial situation changes. However, each refinancing involves: – Application and underwriting fees (though usually waived) – Credit score impact (temporary) – Processing time and documentation

Only refinance if the rate savings justify these costs—typically at least a 0.5% reduction.

Q6: What’s the difference between refinancing and consolidation?

Consolidation (Federal only): – Combines multiple federal loans into one Direct Loan – New rate is the weighted average of existing rates (doesn’t lower your rate) – Preserves federal protections (IDR, PSLF, forbearance) – Takes 2-3 months – No private lender involved

Refinancing (Private only): – Takes out a new private loan to pay off existing loans – New rate is based on your current creditworthiness (can be significantly lower) – Loses federal protections – Takes 2-4 weeks – Involves private lender

Q7: Should I choose a fixed or variable rate?

Choose Fixed Rate if: – You’re keeping the loan 5+ years – You value payment predictability – You’re risk-averse – You have a tight budget

Choose Variable Rate if: – You plan to pay off the loan in 2-3 years – You’re comfortable with interest rate risk – You want the lowest possible initial rate – You have flexible income/budget

For most borrowers, fixed rates are safer and more practical.

Q8: Can I include private loans and federal loans in one refinance?

Yes. When you refinance federal loans with a private lender, you can combine them with private loans into a single new loan. However, this means losing federal protections on those federal loans. Most experts recommend refinancing only private loans if possible.

Q9: Is there a best time of year to refinance?

Market conditions matter more than seasonality. Refinance when: – Rates are favorable (1-2% lower than your current rate) – Your credit score has improved – Your income is stable – You’ve paid down enough debt to improve your debt-to-income ratio

Monitor rates using pre-qualification tools. When you see rates 1% or more below your current rate, that’s typically a good time to refinance.

Q10: What happens if I can’t make a payment after refinancing?

This is critical: Private lenders have far fewer hardship options than federal lenders. If you can’t pay:

– Most private lenders offer 30-90 day forbearance (limited)

– Some offer temporary payment reduction during hardship

– No income-driven options to reduce monthly payments

– Default is possible if you miss 120+ days of payments

This is why refinancing federal loans is risky for those with unstable income. Maintain emergency savings and only refinance if you’re confident in your job security.

Conclusion: Is Refinancing Right for You?

Student loan refinancing in 2026 offers tremendous potential savings—potentially tens of thousands of dollars over your loan life. However, it’s not a one-size-fits-all solution.

Refinance if you: – Have private student loans at high interest rates – Have federal loans and can qualify for rates 1%+ lower – Work in stable employment with strong income – Have no plans to pursue loan forgiveness – Have good credit (670+) to qualify for competitive rates – Want to simplify multiple payments into one

Don’t refinance if you: – Work in public service (PSLF is worth too much) – Expect income fluctuations or job instability – Have low credit scores and can’t qualify for better rates – Need flexible federal repayment options – Plan to pursue any federal loan forgiveness program

Your next steps:

- Assess your situation using the criteria above

- Pre-qualify with 3-5 lenders to see what rates you’d actually receive

- Calculate your potential savings using the actual rates offered

- Compare total costs, not just monthly payments

- Review federal benefits if you have federal loans

- Apply with your chosen lender and complete the refinancing process

Check rates now to see if refinancing makes sense for your specific financial situation. With rates as low as 3.01% available in 2026, qualified borrowers have real opportunities to save substantial money—but only if they make informed decisions based on their personal circumstances and long-term goals.