Finding the best personal loans for bad credit in 2026 can feel overwhelming, but you are not alone. The good news is that lenders have evolved, and securing the best personal loans for bad credit is now easier than ever.

You’re not alone in this, and yes—you can absolutely get a loan in 2026, even with a low credit score. The stress of having bad credit is real, but the good news is that lenders have evolved. Online lenders now look beyond just your credit score and consider factors like your income, employment history, and overall financial profile. This guide walks you through five trusted lenders with high approval odds for bad credit, explains how to boost your chances, and warns you about predatory traps to avoid.

What Qualifies as “Bad Credit”?

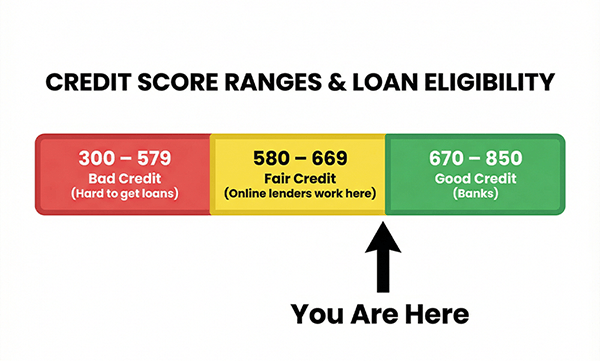

The term “bad credit” typically refers to a FICO score below 630. To understand where you stand, here’s how FICO breaks down the scoring model:

Poor Credit: 300 to 579 — Traditional banks will almost certainly deny you. Lenders see this range as high-risk.

Fair Credit: 580 to 669 — You’re still below average, but online lenders will work with you. Approval odds improve, especially in the upper half of this range.

Why Traditional Banks Say “No” But Online Lenders Say “Yes”

Traditional banks rely heavily on credit scores and follow rigid underwriting rules. If your score doesn’t meet their minimum, they won’t even review your application. Online lenders, however, use alternative underwriting models that incorporate AI technology and non-traditional data like your education, employment history, payment patterns, and income stability. This allows them to approve borrowers who would be instantly rejected by banks.

Reviews of the Best Personal Loans for Bad Credit in 2026

To help you make the right choice, we have reviewed the best personal loans for bad credit available today. These lenders offer high approval odds even if your score is below 630

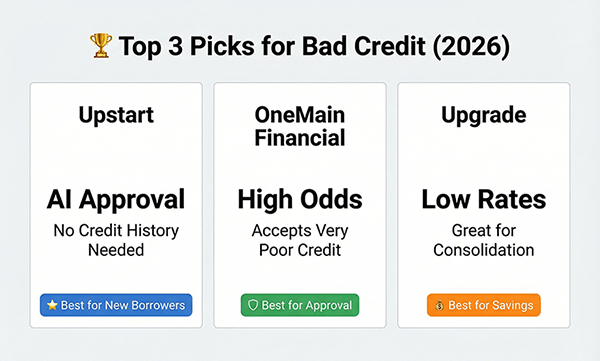

1. Upstart: Best for “Thin” Credit History

Why it stands out: Upstart uses alternative underwriting that goes far beyond your FICO score. The company’s AI algorithm evaluates over 2,500 variables, including your education and employment background.

- Minimum Credit Score: None (as low as 300)

- APR Range: 6.7% – 35.99%

- Loan Amount: $1,000 – $75,000

- Funding Timeline: As fast as 1 day

- Best For: Borrowers with thin credit history, young professionals, students, or anyone rejected by traditional lenders

Key Pro: No minimum credit score requirement means you might qualify even with poor or near-zero credit history.

2. Avant: Best for Scores 600–700

Why it stands out: Avant specializes in fair-to-bad credit and approves borrowers with minimum scores as low as 550. Most of their borrowers have scores between 600–700.

- Minimum Credit Score: 550

- APR Range: 9.95% – 35.99%

- Loan Amount: $2,000 – $40,000

- Funding Timeline: Next business day

- Best For: Borrowers in the fair-to-bad credit range, those needing quick cash

Key Feature: Administration fee of up to 4.75%, deducted from your loan proceeds upfront.

3. Upgrade: Best for Debt Consolidation

Why it stands out: Upgrade shines for consolidating high-interest credit card debt. It offers multiple rate discounts (autopay, direct creditor payment, multiple products) that can save you hundreds in interest.

- Minimum Credit Score: 600 (though typically 580–620)

- APR Range: 8.49% – 35.99%

- Loan Amount: $1,000 – $50,000

- Loan Terms: 24 to 84 months

- Funding Timeline: Next business day for direct deposit; up to 2 weeks if paying creditors directly

- Best For: Consolidating credit card debt, borrowers with fair-to-poor credit who have 3+ years of credit history

Key Feature: Lower credit score requirement than many competitors; origination fee 1.85%–9.99%.

LendingPoint: Best for “Fair” Credit

Why it stands out: LendingPoint uses AI technology to look beyond traditional FICO scores. It considers employment, income, and credit history together.

- Minimum Credit Score: 640

- APR Range: 7.99% – 35.99%

- Loan Amount: $1,000 – $36,500

- Loan Terms: 24 to 72 months

- Funding Timeline: 1 business day

- Best For: Credit-builders, borrowers with 2+ years of credit history, those needing flexible terms

- Income Requirement: Minimum $35,000 annually

Key Feature: Prequalification with no hard credit pull—you can see your rate without damaging your score.

5. OneMain Financial: Best for Very Poor Credit, Highest Approval Odds

Why it stands out: OneMain has no formal minimum credit score requirement and has been lending for over 100 years. They approve borrowers other lenders reject, but rates are higher.

- Minimum Credit Score: None (as low as 600)

- APR Range: 18% – 35.99%

- Loan Amount: $1,500 – $20,000

- Loan Terms: 24–60 months

- Funding Timeline: As soon as 1 hour after closing; up to 2 business days via ACH

- Best For: Very poor credit, those with recent bankruptcy, borrowers who’ve been rejected elsewhere

- Collateral Option: Can secure your loan with an asset (car, savings) to potentially lower your rate

Important Note: OneMain charges origination fees (flat $25–$500 or 1%–10% of loan amount, depending on state) and offers optional insurance products. Read the fine print carefully.

Comparison: The Best Personal Loans for Bad Credit at a Glance

| Lender | Minimum Credit Score | APR Range | Max Loan Amount |

| Upstart | None (as low as 300) | 6.7% – 35.99% | $75,000 |

| Avant | 550 | 9.95% – 35.99% | $40,000 |

| Upgrade | 600 (580–620) | 8.49% – 35.99% | $50,000 |

| LendingPoint | 640 | 7.99% – 35.99% | $36,500 |

| OneMain Financial | None | 18% – 35.99% | $20,000 |

The Truth About “No Credit Check” Loans ( Warning Section)

Unlike risky payday loans, the best personal loans for bad credit come with fixed APRs and clear repayment terms. Always choose a reputable lender over a ‘no credit check’ scam.

Why You Should Avoid Payday Loans

When you’re desperate for cash, “no credit check” loans seem like a miracle. But here’s the hard truth: they’re financial traps.

The Danger: Payday loans charge interest rates of 400% APR or higher—sometimes exceeding 600%. For perspective, if you borrow $500 for two weeks at a typical payday loan rate, you might pay $115 in fees. That’s an annual percentage rate of roughly 1,196% if you kept renewing it.

How the Trap Works:

- Lenders require pre-authorized access to your bank account

- They withdraw payments that don’t cover the full loan or leave principal untouched

- If funds are insufficient, you’re hit with overdraft fees

- Most borrowers get caught in a cycle: nearly 1 in 4 payday loans are re-borrowed 9+ times

The 36% Threshold: Financial experts agree that anything above 36% APR crosses from “affordable credit” into predatory lending. Payday loans blow past this by tenfold or more.

Better Alternatives: Even if your credit is poor, a personal loan from the five lenders above is vastly more affordable. Why? Fixed terms, reasonable repayment schedules, and transparent fees. An APR of 30–35% from Avant or Upgrade is still infinitely better than 400%+ from payday lenders.

Red Flags to Avoid

- “Guaranteed approval”

- “No credit check”

- “Same-day cash”

- “No questions asked”

- Lenders requiring upfront fees

If it sounds too good to be true, it is.

How to Boost Your Approval Odds (Step-by-Step)

Step 1: Check Your Credit Report for Errors

You’d be surprised how often credit bureaus make mistakes. Errors could be killing your score unfairly.

How to do it:

- Visit annualcreditreport.com (free, once per year from each bureau: Experian, Equifax, TransUnion)

- Look for incorrect personal details, accounts you don’t recognize, or payments marked late that you actually made on time

- If you find an error, dispute it directly with the bureau—they must investigate within 30–45 days

Even a single corrected error can boost your score by 20–50 points.

Step 2: Get a Co-Signer (If Possible)

A co-signer is someone with good credit who agrees to repay the loan if you can’t. This dramatically improves your approval odds and may lower your APR by 5–10%.

Who makes a good co-signer?

- Family member or close friend with a FICO score 650+

- Someone willing to take on legal responsibility

Step 3: Show Proof of Steady Income

Lenders want to know you can actually repay the loan. Have these documents ready:

- Recent pay stubs (last 2–3 months)

- Bank statements (last 2–3 months)

- Tax returns (last 1–2 years) if self-employed

- Proof of Social Security or disability benefits (if applicable)

Step 4: Apply for a Smaller Amount First

Instead of requesting $10,000, start with $5,000. Smaller loans have higher approval rates, and successfully repaying builds your credit for future, larger loans.

The Math: A $5,000 approval looks great on your credit report. Once you pay it off, your credit score rises by 30–100 points, and your next application for $10,000+ will have better odds.

FAQ: Questions About the Best Personal Loans for Bad Credit

Q: Can I get a loan with a 500 credit score?

Ans: Yes, but it’s challenging. Upstart and OneMain Financial don’t have minimum credit score requirements, so theoretically you could qualify with a 500 score. However, your approval depends on other factors: income, employment history, debt-to-income ratio, and whether you have a co-signer. Expect higher APRs and potentially smaller loan amounts if approved.

Q: How fast can I get the funds?

Ans: Online lenders are fastest. Most approve within 1–3 business days and fund within 1–5 business days after approval. Upstart and OneMain Financial advertise same-day to 24-hour funding for approved borrowers. Even in the fastest cases, allow 1–2 business days for the money to appear in your account due to banking processing times.

Q: Will checking my rate hurt my credit score? (Soft Pull vs. Hard Pull)

Ans: This is critical to understand. When you check your rate with most lenders (Upstart, Avant, LendingPoint, Upgrade), they perform a soft credit pull to give you a prequalification estimate. A soft pull does not impact your credit score and doesn’t show up on your credit report to other lenders.

Hard Pull: This happens when you formally apply for the loan. A hard pull can temporarily lower your credit score by 5–10 points, but the impact typically fades within 6–12 months.

Pro Tip: You can safely compare rates from multiple lenders using soft pulls. When comparing, multiple hard pulls for the same type of credit (personal loans) within 14–45 days usually count as a single inquiry, minimizing credit damage.

Q: What if I’m denied?

Ans: Don’t give up. Try these steps:

1: Wait 30 days and reapply (your credit report updates monthly)

2: Apply with a co-signer

3: Apply with a smaller loan amount

4: Build your credit for 3–6 months, then reapply

5: Consider a credit builder loan from your bank or credit union

Q: Are there any guaranteed approval lenders?

Ans: No. Any lender claiming “guaranteed approval” is either lying or running a scam. Even alternative lenders use underwriting criteria. What’s different is that online lenders consider more than just your credit score.

Q: Can I get a loan with a 500 credit score?

Even with a 500 score, applying for the best personal loans for bad credit (like Upstart) is safer than choosing payday lenders.

Final Thoughts on the Best Personal Loans for Bad Credit

Having a low credit score feels isolating, but the lending landscape has changed dramatically. You’re not locked out of credit. Upstart, Avant, Upgrade, LendingPoint, and OneMain Financial all approve borrowers with poor credit, offering real loans with fixed terms and transparent fees—nothing predatory.

Your Next Steps

- Check your credit report for errors and dispute any you find

- Get prequalified with 2–3 lenders using soft pulls (no score damage)

- Compare their actual offers, not just APR ranges

- Apply with the best lender for your situation

- Use the funds responsibly and make on-time payments—building good credit for your future

You’ve got this. Thousands of Americans with bad credit successfully get loans every day. There’s no shame in where your credit stands now—only strength in taking action to improve it.

Ultimately, applying for one of the best personal loans for bad credit is a smart step toward rebuilding your financial future. Compare your offers carefully and pick the one that fits your budget.